The manufacturing economy has faced a series of challenges over the past three years, constricting growth of the precision gearbox market. However, to generate additional revenue streams, precision gearbox manufacturers have been taking proactive measures. This insight explores the key strategies manufacturers are adopting to drive momentum during challenging times and prepare for the next wave of market expansion.

These strategies include expanding product portfolios, pursuing vertical integration through acquisitions, and establishing localized operations.

1. Providing Sensorized Solutions for Robotics Clients

Manufacturers are diversifying their value propositions by offering solution-type products with additional sensors, targeted at improving product performance and reducing clients’ integration efforts.

The continued expansion of the robotics industry has fueled the demand for sensorized gearboxes and actuator solutions. Emerging companies in the sector are increasingly seeking solution packages for actuators, and precision gearbox suppliers are responding by developing tailored products. Leading manufacturers like Nabtesco, Harmonic Drive, and Nidec have all launched precision gearboxes or geared motors with built-in sensors, specifically targeting the robotics market.

The growing market for cobots (collaborative robots) and humanoid robots is a key driver of demand for sensorized precision gear solutions. As cobots are deployed in more delicate tasks like polishing and precise assembly, demand for sensor-equipped cobots has been growing. While not all cobot axes come with sensors, every humanoid robot actuator typically requires torque sensors for safety and precise control.

2. Enhancing Software Offerings

In addition to hardware, monitoring software solutions and predictive maintenance functions are seeing a rise in demand from precision gearbox clients.

Frequently offered with sensors as a package solution, monitoring software is used for analyzing critical data provided by sensors attached to precision gear products, optimizing gearbox performance, and ensuring precise control. This technology is especially important in industries that rely on machines and gearboxes operating continuously, where unplanned downtime can be costly. Key sectors driving this demand include automotive and logistics.

Gearbox suppliers are investing in software solutions to meet these needs. For example, Nabtesco introduced “virtual sensors” integrated with gearboxes—a software solution designed to analyze torque and speed parameters. This technology enables condition monitoring and predictive maintenance without requiring physical sensor hardware.

3. Vertical Integration Along the Supply Chain Through Acquisition

In addition to investing in internal R&D, manufacturers are expanding their product offerings through strategic acquisitions, aimed at meeting a broader range of market demands and increasing competitiveness.

For example, Wittenstein’s recent acquisition of motion control supplier STXI Motion highlights the growing trend of vertical integration in the precision gearbox industry. Combining Wittenstein’s expertise in precision gearboxes with STXI Motion’s motion control technology is expected to enhance the company’s development of integrated actuator solutions, which are increasingly popular in the mobile robotics sector.

Back in 2022, Schaeffler’s acquisition of Melior Motion expanded its product offering for robotics gearboxes. This enabled the company to rapidly gain market share in the robotics industry and positioned Schaeffler to move further into the fast-growing humanoid robot sector.

4. Establishing Localized Operations

To better serve their customers, improve responsiveness, provide faster delivery, and reduce costs, precision gearbox manufacturers are setting up production and service centers closer to key markets.

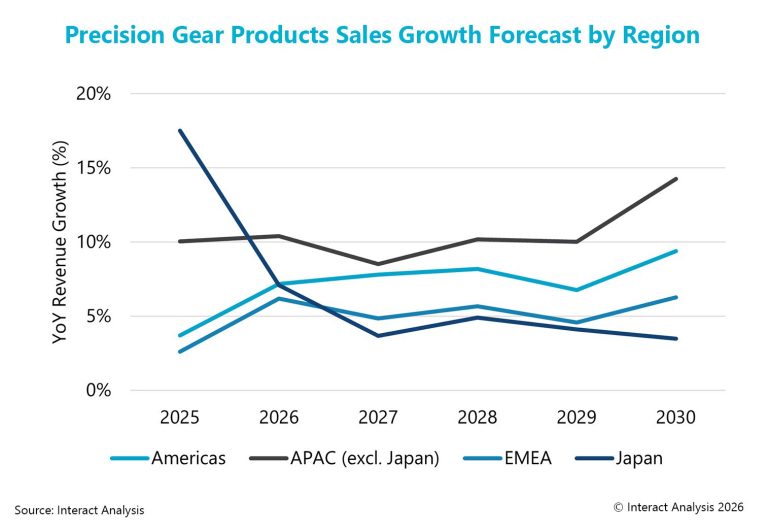

The Asia-Pacific and Americas markets are particularly attractive for manufacturers looking to establish localized operations. This strategy aligns with forecasts suggesting higher growth in these regions over the next five years. Increasing production of robots, as well as semiconductor and electronics machinery, is driving this growth.

Examples include:

- Schaeffler announced a new subsidiary in China focused on humanoid robot bearings and gearboxes

- Leaderdrive partnered with Tier 1 automotive supplier Minth Group in the US to set up a US-based assembly facility for humanoid robot actuators

- In late 2024, Nidec started production of strain wave gearboxes in China, targeting the local robotics market

Final Thoughts

The move toward sensorized products and software-driven functionality signals a clear convergence between mechanical engineering and digital capabilities. The gearbox is evolving from a passive component into an active data-generating asset. Companies that can successfully bridge this hardware-software divide are likely to present stronger differentiation, while those that remain purely hardware-focused risk being pushed toward commoditization.

Precision gearbox manufacturers are repositioning themselves as system-level enablers in the robotics ecosystem, rather than pure component suppliers. This shift is not just a defensive response to a volatile manufacturing environment—it reflects a deeper recognition that future value will concentrate around integration, digital intelligence, and proximity to the end user.